Exponential Economist Meets Finite Physicist

Today’s guest post in our Limits to Growth 40th anniversary series is courtesy of Tom Murphy. Tom is an associate professor of physics at the University of California, San Diego. He has simultaneously posted this entertaining conversation on his popular blog, Do the Math. More about Tom after the conversation. While there are economists, like Herman Daly, who believe there are limits to economic growth, there are many more, such as the infamous Julian Simon, who do not. That ratio is, I believe, in the process of changing. We hear from both Daly and the late Simon in the GrowthBusters film. It’s pretty entertaining. But I have to hand it to Tom Murphy. He shares with us here an enlightening and engaging conversation with an economist of Simon’s ilk. Enjoy and learn! – Dave Gardner

Exponential Economist Meets Finite Physicist

by Tom Murphy

Some while back, I found myself sitting next to an accomplished economics professor at a dinner event. Shortly after pleasantries, I said to him, “economic growth cannot continue indefinitely,” just to see where things would go. It was a lively and informative conversation. I was somewhat alarmed by the disconnect between economic theory and physical constraints—not for the first time, but here it was up-close and personal. Though my memory is not keen enough to recount our conversation verbatim, I thought I would at least try to capture the key points and convey the essence of the tennis match—with some entertainment value thrown in.

Cast of characters: Physicist, played by me; Economist, played by an established economics professor from a prestigious institution. Scene: banquet dinner, played in four acts (courses).

Note: because I have a better retention of my own thoughts than those of my conversational companion, this recreation is lopsided to represent my own points/words. So while it may look like a physicist-dominated conversation, this is more an artifact of my own recall capabilities. I also should say that the other people at our table were not paying attention to our conversation, so I don’t know what makes me think this will be interesting to readers if it wasn’t even interesting enough to others at the table! But here goes…

Act One: Bread and Butter

Physicist: Hi, I’m Tom. I’m a physicist.

Economist: Hi Tom, I’m [ahem..cough]. I’m an economist.

Physicist: Hey, that’s great. I’ve been thinking a bit about growth and want to run an idea by you. I claim that economic growth cannot continue indefinitely.

Economist: [chokes on bread crumb] Did I hear you right? Did you say that growth can not continue forever?

Physicist: That’s right. I think physical limits assert themselves.

Economist: Well sure, nothing truly lasts forever. The sun, for instance, will not burn forever. On the billions-of-years timescale, things come to an end.

Physicist: Granted, but I’m talking about a more immediate timescale, here on Earth. Earth’s physical resources—particularly energy—are limited and may prohibit continued growth within centuries, or possibly much shorter depending on the choices we make. There are thermodynamic issues as well.

Economist: I don’t think energy will ever be a limiting factor to economic growth. Sure, conventional fossil fuels are finite. But we can substitute non-conventional resources like tar sands, oil shale, shale gas, etc. By the time these run out, we’ll likely have built up a renewable infrastructure of wind, solar, and geothermal energy—plus next-generation nuclear fission and potentially nuclear fusion. And there are likely energy technologies we cannot yet fathom in the farther future.

Physicist: Sure, those things could happen, and I hope they do at some non-trivial scale. But let’s look at the physical implications of the energy scale expanding into the future. So what’s a typical rate of annual energy growth over the last few centuries?

Economist: I would guess a few percent. Less than 5%, but at least 2%, I should think.

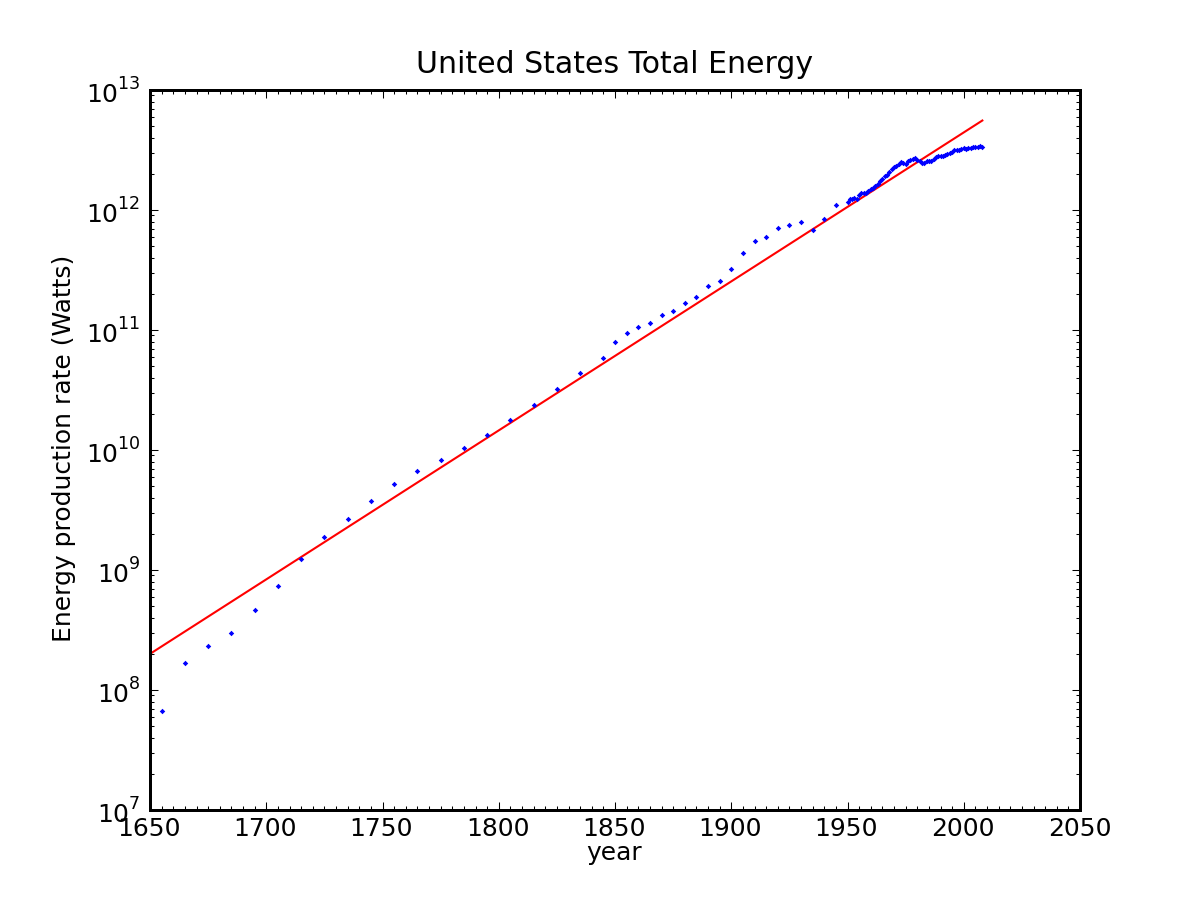

Physicist: Right, if you plot the U.S. energy consumption in all forms from 1650 until now, you see a phenomenally faithful exponential at about 3% per year over that whole span. The situation for the whole world is similar. So how long do you think we might be able to continue this trend?

Economist: Well, let’s see. A 3% growth rate means a doubling time of something like 23 years. So each century might see something like a 15–20× increase. I see where you’re going. A few more centuries like that would perhaps be absurd. But don’t forget that population was increasing during centuries past—the period on which you base your growth rate. Population will stop growing before more centuries roll by.

Physicist: True enough. So we would likely agree that energy growth will not continue indefinitely. But two points before we continue: First, I’ll just mention that energy growth has far outstripped population growth, so that per-capita energy use has surged dramatically over time—our energy lives today are far richer than those of our great-great-grandparents a century ago [economist nods]. So even if population stabilizes, we are accustomed to per-capita energy growth: total energy would have to continue growing to maintain such a trend [another nod].

Second, thermodynamic limits impose a cap to energy growth lest we cook ourselves. I’m not talking about global warming, CO2 build-up, etc. I’m talking about radiating the spent energy into space. I assume you’re happy to confine our conversation to Earth, foregoing the spectre of an exodus to space, colonizing planets, living the Star Trek life, etc.

Economist: More than happy to keep our discussion grounded to Earth.

Physicist: [sigh of relief: not a space cadet] Alright, the Earth has only one mechanism for releasing heat to space, and that’s via (infrared) radiation. We understand the phenomenon perfectly well, and can predict the surface temperature of the planet as a function of how much energy the human race produces. The upshot is that at a 2.3% growth rate (conveniently chosen to represent a 10× increase every century), we would reach boiling temperature in about 400 years. [Pained expression from economist.] And this statement is independent of technology. Even if we don’t have a name for the energy source yet, as long as it obeys thermodynamics, we cook ourselves with perpetual energy increase.

Economist: That’s a striking result. Could not technology pipe or beam the heat elsewhere, rather than relying on thermal radiation?

Physicist: Well, we could (and do, somewhat) beam non-thermal radiation into space, like light, lasers, radio waves, etc. But the problem is that these “sources” are forms of high-grade, low-entropy energy. Instead, we’re talking about getting rid of the waste heat from all the processes by which we use energy. This energy is thermal in nature. We might be able to scoop up some of this to do useful “work,” but at very low thermodynamic efficiency. If you want to use high-grade energy in the first place, having high-entropy waste heat is pretty inescapable.

Economist: [furrowed brow] Okay, but I still think our path can easily accommodate at least a steady energy profile. We’ll use it more efficiently and for new pursuits that continue to support growth.

Physicist: Before we tackle that, we’re too close to an astounding point for me to leave it unspoken. At that 2.3% growth rate, we would be using energy at a rate corresponding to the total solar input striking Earth in a little over 400 years. We would consume something comparable to the entire sun in 1400 years from now. By 2500 years, we would use energy at the rate of the entire Milky Way galaxy—100 billion stars! I think you can see the absurdity of continued energy growth. 2500 years is not that long, from a historical perspective. We know what we were doing 2500 years ago. I think I know what we’re not going to be doing 2500 years hence.

Economist: That’s really remarkable—I appreciate the detour. You said about 1400 years to reach parity with solar output?

Physicist: Right. And you can see the thermodynamic point in this scenario as well. If we tried to generate energy at a rate commensurate with that of the Sun in 1400 years, and did this on Earth, physics demands that the surface of the Earth must be hotter than the (much larger) surface of the Sun. Just like 100 W from a light bulb results in a much hotter surface than the same 100 W you and I generate via metabolism, spread out across a much larger surface area.

Economist: I see. That does make sense.

Act Two: Salad

Economist: So I’m as convinced as I need to be that growth in raw energy use is a limited proposition—that we must one day at the very least stabilize to a roughly constant yearly expenditure. At least I’m willing to accept that as a starting point for discussing the long term prospects for economic growth. But coming back to your first statement, I don’t see that this threatens the indefinite continuance of economic growth.

For one thing, we can keep energy use fixed and still do more with it in each passing year via efficiency improvements. Innovations bring new ideas to the market, spurring investment, market demand, etc. These are things that will not run dry. We have plenty of examples of fundamentally important resources in decline, only to be substituted or rendered obsolete by innovations in another direction.

Physicist: Yes, all these things happen, and will continue at some level. But I am not convinced that they represent limitless resources.

Economist: Do you think ingenuity has a limit—that the human mind itself is only so capable? That could be true, but we can’t credibly predict how close we might be to such a limit.

Physicist: That’s not really what I have in mind. Let’s take efficiency first. It is true that, over time, cars get better mileage, refrigerators use less energy, buildings are built more smartly to conserve energy, etc. The best examples tend to see factor-of-two improvements on a 35 year timeframe, translating to 2% per year. But many things are already as efficient as we can expect them to be. Electric motors are a good example, at 90% efficiency. It will always take 4184 Joules to heat a liter of water one degree Celsius. In the middle range, we have giant consumers of energy—like power plants—improving much more slowly, at 1% per year or less. And these middling things tend to be something like 30% efficient. How many more “doublings” are possible? If many of our devices were 0.01% efficient, I would be more enthusiastic about centuries of efficiency-based growth ahead of us. But we may only have one more doubling in us, taking less than a century to realize.

Economist: Okay, point taken. But there is more to efficiency than incremental improvement. There are also game-changers. Tele-conferencing instead of air travel. Laptop replaces desktop; iPhone replaces laptop, etc.—each far more energy frugal than the last. The internet is an example of an enabling innovation that changes the way we use energy.

Physicist: These are important examples, and I do expect some continuation along this line, but we still need to eat, and no activity can get away from energy use entirely. [semi-reluctant nod/bobble] Sure, there are lower-intensity activities, but nothing of economic value is completely free of energy.

Economist: Some things can get awfully close. Consider virtualization. Imagine that in the future, we could all own virtual mansions and have our every need satisfied: all by stimulative neurological trickery. We would stil need nutrition, but the energy required to experience a high-energy lifestyle would be relatively minor. This is an example of enabling technology that obviates the need to engage in energy-intensive activities. Want to spend the weekend in Paris? You can do it without getting out of your chair. [More like an IV-drip-equipped toilet than a chair, the physicist thinks.]

Physicist: I see. But this is still a finite expenditure of energy per person. Not only does it take energy to feed the person (today at a rate of 10 kilocalories of energy input per kilocalorie eaten, no less), but the virtual environment probably also requires a supercomputer—by today’s standards—for every virtual voyager. The supercomputer at UCSD consumes something like 5 MW of power. Granted, we can expect improvement on this end, but today’s supercomputer eats 50,000 times as much as a person does, so there is a big gulf to cross. I’ll take some convincing. Plus, not everyone will want to live this virtual existence.

Economist: Really? Who could refuse it? All your needs met and an extravagant lifestyle—what’s not to like? I hope I can live like that myself someday.

Physicist: Not me. I suspect many would prefer the smell of real flowers—complete with aphids and sneezing; the feel of real wind messing up their hair; even real rain, real bee-stings, and all the rest. You might be able to simulate all these things, but not everyone will want to live an artificial life. And as long as there are any holdouts, the plan of squeezing energy requirements to some arbitrarily low level fails. Not to mention meeting fixed bio-energy needs.

Act Three: Main Course

Physicist: But let’s leave the Matrix, and cut to the chase. Let’s imagine a world of steady population and steady energy use. I think we’ve both agreed on these physically-imposed parameters. If the flow of energy is fixed, but we posit continued economic growth, then GDP continues to grow while energy remains at a fixed scale. This means that energy—a physically-constrained resource, mind—must become arbitrarily cheap as GDP continues to grow and leave energy in the dust.

Economist: Yes, I think energy plays a diminishing role in the economy and becomes too cheap to worry about.

Physicist: Wow. Do you really believe that? A physically limited resource (read scarcity) that is fundamental to every economic activity becomes arbitrarily cheap? [turns attention to food on the plate, somewhat stunned]

Economist: [after pause to consider] Yes, I do believe that.

Physicist: Okay, so let’s be clear that we’re talking about the same thing. Energy today is roughly 10% of GDP. Let’s say we cap the physical amount available each year at some level, but allow GDP to keep growing. We need to ignore inflation as a nuisance in this case: if my 10 units of energy this year costs $10,000 out of my $100,000 income; then next year that same amount of energy costs $11,000 and I make $110,000—I want to ignore such an effect as “meaningless” inflation: the GDP “growth” in this sense is not real growth, but just a re-scaling of the value of money.

Economist: Agreed.

Physicist: Then in order to have real GDP growth on top of flat energy, the fractional cost of energy goes down relative to the GDP as a whole.

Economist: Correct.

Physicist: How far do you imagine this can go? Will energy get to 1% of GDP? 0.1%? Is there a limit?

Economist: There does not need to be. Energy may become of secondary importance in the economy of the future—like in the virtual world I illustrated.

Physicist: But if energy became arbitrarily cheap, someone could buy all of it, and suddenly the activities that comprise the economy would grind to a halt. Food would stop arriving at the plate without energy for purchase, so people would pay attention to this. Someone would be willing to pay more for it. Everyone would. There will be a floor to how low energy prices can go as a fraction of GDP.

Economist: That floor may be very low: much lower than the 5–10% we pay today.

Physicist: But is there a floor? How low are you willing to take it? 5%? 2%? 1%?

Economist: Let’s say 1%.

Physicist: So once our fixed annual energy costs 1% of GDP, the 99% remaining will find itself stuck. If it tries to grow, energy prices must grow in proportion and we have monetary inflation, but no real growth.

Economist: Well, I wouldn’t go that far. You can still have growth without increasing GDP.

Physicist: But it seems that you are now sold on the notion that the cost of energy would not naturally sink to arbitrarily low levels.

Economist: Yes, I have to retract that statement. If energy is indeed capped at a steady annual amount, then it is important enough to other economic activities that it would not be allowed to slip into economic obscurity.

Physicist: Even early economists like Adam Smith foresaw economic growth as a temporary phase lasting maybe a few hundred years, ultimately limited by land (which is where energy was obtained in that day). If humans are successful in the long term, it is clear that a steady-state economic theory will far outlive the transient growth-based economic frameworks of today. Forget Smith, Keynes, Friedman, and that lot. The economists who devise a functioning steady-state economic system stand to be remembered for a longer eternity than the growth dudes. [Economist stares into the distance as he contemplates this alluring thought.]

Act Four: Dessert

Economist: But I have to object to the statement that growth must stop once energy amount/price saturates. There will always be innovations that people are willing to purchase that do not require additional energy.

Physicist: Things will certainly change. By “steady-state,” I don’t mean static. Fads and fashions will always be part of what we do—we’re not about to stop being human. But I’m thinking more of a zero-sum game here. Fads come and go. Some fraction of GDP will always go toward the fad/innovation/gizmo of the day, but while one fad grows, another fades and withers. Innovation therefore will maintain a certain flow in the economy, but not necessarily growth.

Economist: Ah, but the key question is whether life 400 years from now is undeniably of higher quality than life today. Even if energy is fixed, and GDP is fixed once the cost of energy saturates at the lower bound, will quality of life continue to improve in objectively agreed-upon ways?

Physicist: I don’t know how objective such an assessment can be. Many today yearn for days past. Maybe this is borne of ignorance or romanticism over the past (1950′s often comes up). It may be really exciting to imagine living in Renaissance Europe, until a bucket of nightsoil hurled from a window splatters off the cobblestone and onto your breeches. In any case, what kind of universal, objective improvements might you imagine?

Economist: Well, for instance, look at this dessert, with its decorative syrup swirls on the plate. It is marvelous to behold.

Physicist: And tasty.

Economist: We value such desserts more than plain, unadorned varieties. In fact, we can imagine an equivalent dessert with equivalent ingredients, but the decorative syrup unceremoniously pooled off to one side. We value the decorated version more. And the chefs will continue to innovate. Imagine a preparation/presentation 400 years from now that would blow your mind—you never thought dessert could be made to look so amazing and taste so delectably good. People would line the streets to get hold of such a creation. No more energy, no more ingredients, yet of increased value to society. That’s a form of quality of life improvement, requiring no additional resources, and perhaps costing the same fraction of GDP, or income.

Physicist: I’m smiling because this reminds me of a related story. I was observing at Palomar Observatory with an amazing instrumentation guru named Keith who taught me much. Keith’s night lunch—prepared in the evening by the observatory kitchen and placed in a brown bag—was a tuna-fish sandwich in two parts: bread slices in a plastic baggie, and the tuna salad in a small plastic container (so the tuna would not make the bread soggy after hours in the bag). Keith plopped the tuna onto the bread in an inverted container-shaped lump, then put the other piece of bread on top without first spreading the tuna. It looked like a snake had just eaten a rat. Perplexed, I asked if he intended to spread the tuna before eating it. He looked at me quizzically (like Morpheus in the Matrix: “You think that’s air you’re breathing? Hmm.”), and said—memorably, “It all goes in the same place.”

My point is that the stunning presentation of desserts will not have universal value to society. It all goes in the same place, after all. [I’ll share a little-known secret. It’s hard to beat a Hostess Ding Dong for dessert. At 5% the cost of fancy desserts, it’s not clear how much value the fancy things add.]

After-Dinner Contemplations

The evening’s after-dinner keynote speech began, so we had to shelve the conversation. Reflecting on it, I kept thinking, “This should not have happened. A prominent economist should not have to walk back statements about the fundamental nature of growth when talking to a scientist with no formal economics training.” But as the evening progressed, the original space in which the economist roamed got painted smaller and smaller.

First, he had to acknowledge that energy may see physical limits. I don’t think that was part of his initial virtual mansion.

Next, the efficiency argument had to shift away from straight-up improvements to transformational technologies. Virtual reality played a prominent role in this line of argument.

Finally, even having accepted the limits to energy growth, he initially believed this would prove to be of little consequence to the greater economy. But he had to ultimately admit to a floor on energy price and therefore an end to traditional growth in GDP—against a backdrop fixed energy.

I got the sense that this economist’s view on growth met some serious challenges during the course of the meal. Maybe he was not putting forth the most coherent arguments that he could have made. But he was very sharp and by all measures seemed to be at the top of his game. I choose to interpret the episode as illuminating a blind spot in traditional economic thinking. There is too little acknowledgement of physical limits, and even the non-compliant nature of humans, who may make choices we might think to be irrational—just to remain independent and unencumbered.

I recently was motivated to read a real economics textbook: one written by people who understand and respect physical limitations. The book, called Ecological Economics, by Herman Daly and Joshua Farley, states in its Note to Instructors:

…we do not share the view of many of our economics colleagues that growth will solve the economic problem, that narrow self-interest is the only dependable human motive, that technology will always find a substitute for any depleted resource, that the market can efficiently allocate all types of goods, that free markets always lead to an equilibrium balancing supply and demand, or that the laws of thermodynamics are irrelevant to economics.

This is a book for me!

Epilogue

The conversation recreated here did challenge my own understanding as well. I spent the rest of the evening pondering the question: “Under a model in which GDP is fixed—under conditions of stable energy, stable population, steady-state economy: if we accumulate knowledge, improve the quality of life, and thus create an unambiguously more desirable world within which to live, doesn’t this constitute a form of economic growth?”

I had to concede that yes—it does. This often falls under the title of “development” rather than “growth.” I ran into the economist the next day and we continued the conversation, wrapping up loose ends that were cut short by the keynote speech. I related to him my still-forming position that yes, we can continue tweaking quality of life under a steady regime. I don’t think I ever would have explicitly thought otherwise, but I did not consider this to be a form of economic growth. One way to frame it is by asking if future people living in a steady-state economy—yet separated by 400 years—would always make the same, obvious trades? Would the future life be objectively better, even for the same energy, same GDP, same income, etc.? If the answer is yes, then the far-future person gets more for their money: more for their energy outlay. Can this continue indefinitely (thousands of years)? Perhaps. Will it be at the 2% per year level (factor of ten better every 100 years)? I doubt that.

So I can twist my head into thinking of quality of life development in an otherwise steady-state as being a form of indefinite growth. But it’s not your father’s growth. It’s not growing GDP, growing energy use, interest on bank accounts, loans, fractional reserve money, investment. It’s a whole different ballgame, folks. Of that, I am convinced. Big changes await us. An unrecognizable economy. The main lesson for me is that growth is not a “good quantum number,” as physicists will say: it’s not an invariant of our world. Cling to it at your own peril.

Note: This conversation is my contribution to a series at www.growthbusters.org honoring the 40th anniversary of the Limits to Growth study. You can explore the series here. Also see my previous reflection on the Limits to Growth work. You may also be interested in checking out and signing the Pledge to Think Small and consider organizing an Earth Day weekend house party screening of the GrowthBusters movie.

Tom Murphy

Tom Murphy is an associate professor of physics at the University of California, San Diego. Murphy’s keen interest in energy topics began with his teaching a course on energy and the environment for non-science majors at UCSD. Motivated by the unprecedented challenges we face, he has applied his instrumentation skills to exploring alternative energy and associated measurement schemes. Following his natural instincts to educate, Murphy is eager to get people thinking about the quantitatively convincing case that our pursuit of an ever-bigger scale of life faces gigantic challenges and carries significant risks. He does this largely through his very popular blog, Do the Math. This conversation was simultaneously published here at Do the Math.

Trackback from your site.

jason dow

| #

Thank you

Brilliant conversation. In my conversations around similar yopics i found that a cultural shadow at play shading areas of possible insight and feel this conversation has illustrated a disconnect between what is true and what we want to be true…

I will share this with friends

Cheers

Jason

Reply

JC

| #

Well Tom, you were certainly not afraid to let the economist see the absurdity of his learned assumptions but why talk steady state? You let him off easy.

With an economy that consumes finite, non-renewable resource there is no such thing as steady state; decline is inevitable, and due to the nature of the exponential function, sooner that most would ever imagine. I don’t believe that the theoretical approach is appropriate here. In fact, it is that very method of thinking that has put us in the unenviable position we now find ourselves. By assuming that some new idea will solve our current problems only encourages the status quo.

The reality is that petroleum is the greatest energy source that we have, or are likely to have, in the pertinent future, due to it’s relative abundance, density, and convenience. Given our almost complete dependence on it, even with it’s decline it will remain preeminent for at least several decades. I would have been interested to have heard his assessment of the impact of ever increasing energy costs during this phase rather that the very low probability outcome described in the conversation. I fear that such a scenario would have been beyond his comprehension. However, the non-linear relationship between price and demand has been in effect for some time now as demand increases but supply becomes relatively inelastic. (On a related note, demand is often misunderstood. Demand is not what you want but what you can pay for). Only an economist could pretend that such a significant change was of little importance. It is shocking that economic theory is so inaccurate, and even more so that economists are seemingly unaware of this inaccuracy.

The problem is that any attempt to describe a complex system statistically requires certain assumptions concerning said system. In economics one of the primary failures is the assumption of independence of variables. By attempting to evaluate such a fantastically complicated system by analyzing a limited number of parameters of a limited number of individual components while ignoring the interactions of those components leads to a grossly inadequate understanding of the performance of the system as a whole (and yet we continue to use these ideas to build policy!). To coin a phrase, the devil is in the emergent properties.

Economists are spectacularly unable to anticipate dramatic changes because their models and theories function only in an essentially static environment. That these models have performed reasonably well for some time says much more about the relatively homogeneity (growth, growth, and more growth!) of the recent past than it does about the ability of the models to describe the dynamic world in which we live. The flip side of that argument is that the huge divergence of economic theory and economic reality is evidence of just how large and rare an event we are at the inception of.

Cheers, JC

Reply

Rupert Russell

| #

An excellent piece, thank you for these insights. It is a debate that should be conducted on a much larger stage; this may take time.

One thing that should also feature centrally in discussions of this nature is the end of the waged labour paradigm and diminishing purchasing power due to automation and mechanisation. It is all part of the same problem and cannot be solved with outdated methods of economic understanding.

Reply